Revenue Sharing vs. Traditional Loans for Creators

Is revenue sharing better than a traditional loan for Creators?

Revenue sharing differs from loans by having no fixed repayments - distributions to investors are based on actual revenue. If revenue is lower, payments are lower, reducing pressure compared to fixed loan obligations.

Educational Content: This content is for educational purposes only and does not constitute investment advice. All investments involve risk, including potential loss of principal. See full disclosures.

What Is Revenue Sharing?

Revenue sharing is a funding model in which a Creator raises capital by agreeing to share a defined percentage of future revenue with Investors for a specified period. Unlike a loan, there is no principal to repay, no interest rate, and no fixed monthly payment. The obligation is proportional: when revenue is higher, Investors receive more; when revenue is lower, Investors receive less.

In the context of YouTube Creators, GigaStar has built a structured, SEC-registered version of this model through Channel Revenue Tokens (CRTs). Here is how it works: a Creator applies to GigaStar and, if accepted, issues CRTs through an offering conducted under SEC Regulation Crowdfunding (Reg CF). The offering is documented in a Form C, the SEC-required disclosure document that specifies the revenue-sharing percentage, the term length, the amount being raised, risk factors, and use of proceeds. The offering is hosted on GigaStar Market, an SEC-registered funding portal and FINRA member, where everyday Investors can review the Creator's channel data and decide whether to participate.

Once the offering closes and the Creator receives the capital, the revenue-sharing period begins. YouTube pays the Creator through its standard AdSense process. GigaStar then calculates each CRT holder's proportional share of the Creator's YouTube revenue based on the terms in the Form C and distributes funds monthly to Investor accounts.

The defining characteristic of this model is variability. There is no fixed amount due each month. If a Creator's channel has a strong Q4 with elevated CPM rates and higher viewership, distributions increase. If Q1 brings a seasonal dip — as it typically does across YouTube — distributions decrease. The Creator's obligation adjusts in real time with actual performance, rather than remaining fixed against it.

This structure fundamentally changes the relationship between a Creator and their capital source. Rather than a creditor-debtor dynamic where the Creator owes a fixed amount regardless of circumstances, revenue sharing creates an alignment of interests: Investors participate in the Creator's actual performance, for better or worse, and the Creator's cash flow obligations flex with reality rather than fighting against it.

For Creators interested in exploring this model, applications are available at apply.gigastarmarket.io.

How Traditional Loans Work

A traditional business loan is a debt instrument. You borrow a fixed sum from a lender — typically a bank, credit union, or the Small Business Administration (SBA) — and agree to repay that sum, plus interest, over a defined schedule. The monthly payment amount is determined at the outset and does not change based on your revenue performance.

The lending process begins with an application. The lender evaluates your creditworthiness through a combination of factors: personal and business credit scores, revenue history, existing debt, collateral available to secure the loan, and a business plan that demonstrates your ability to repay. For traditional banks, this evaluation process can take weeks or months and often requires extensive documentation — tax filings, income statements, balance sheets, and projections.

If approved, you receive the loan proceeds as a lump sum and begin making regular payments according to a fixed amortization schedule. A typical small business loan might carry an interest rate between 6% and 13%, with a repayment term of three to seven years. SBA loans, which are partially backed by the federal government, tend to offer more favorable rates but have their own qualification requirements and a lengthy approval process.

The fundamental feature of a loan is predictability. Both the lender and the borrower know exactly what is owed each month. The payment is the same whether your channel earned $20,000 or $2,000 in YouTube revenue that month. Once all payments are made and the principal plus interest is fully repaid, the obligation ends completely. There is no ongoing relationship, no revenue share, and no continued financial connection.

However, this predictability creates a tension for Creators. YouTube revenue is inherently variable — it fluctuates with viewership, ad market conditions, seasonal CPM cycles, algorithm changes, and content performance. A fixed loan payment that is comfortable during a strong month can become a significant burden during a slow one. And unlike a retail business that might have inventory or equipment to pledge as collateral, most Creators have intangible assets that traditional lenders do not know how to value.

The practical reality is that most banks decline loan applications from content Creators. The business model is unfamiliar to traditional underwriters, the revenue streams are nonstandard, and the collateral is insufficient by conventional standards. This is the gap that alternative funding models — including revenue-sharing crowdfunding — were created to fill.

Side-by-Side Comparison

The following table compares the structural features of revenue sharing through CRTs and traditional business loans across the dimensions that matter most to Creators making a funding decision.

| Factor | Revenue Sharing (CRTs) | Traditional Loan |

|---|---|---|

| Repayment Structure | Percentage of actual YouTube revenue, distributed monthly | Fixed monthly payments of principal + interest |

| Cash Flow Impact | Variable — scales with revenue. Lower revenue months mean lower obligations | Fixed — same payment regardless of revenue performance |

| Ownership | None transferred. CRTs are not equity; Creator retains full ownership and creative control | None transferred. Lender has no ownership stake |

| Credit Requirements | Based on channel performance metrics, not personal credit score | Heavily dependent on personal and/or business credit score |

| Collateral | None required | Often required — personal assets, equipment, or other business assets |

| Total Cost | Depends on actual revenue over the full term; scales proportionally | Defined at origination; total principal + interest is calculable upfront |

| Flexibility | Full creative control; no content restrictions | Generally no content restrictions, but covenants may apply |

| Term Structure | Revenue-sharing percentage for a defined number of years | Fixed repayment period (typically 3-7 years) |

| Regulatory Framework | SEC Regulation Crowdfunding; Form C filing; FINRA-member funding portal | Banking regulations; consumer lending laws |

| Default Risk | No traditional default — obligation is to share revenue, not make a fixed payment | Default occurs if fixed payments are missed; can affect credit score and trigger collateral seizure |

| Accessibility | Available to qualifying Creators regardless of traditional credit profile | Often inaccessible to Creators due to unfamiliar business model and lack of traditional collateral |

This comparison highlights a structural difference in how each model handles uncertainty. Loans push revenue risk onto the Creator: you owe the same amount regardless of what happens. Revenue sharing distributes that risk between Creator and Investor: both sides participate in the actual performance of the channel.

Cash Flow Differences: Fixed vs. Variable

Understanding how each funding model interacts with a Creator's cash flow is essential, because YouTube revenue is anything but steady.

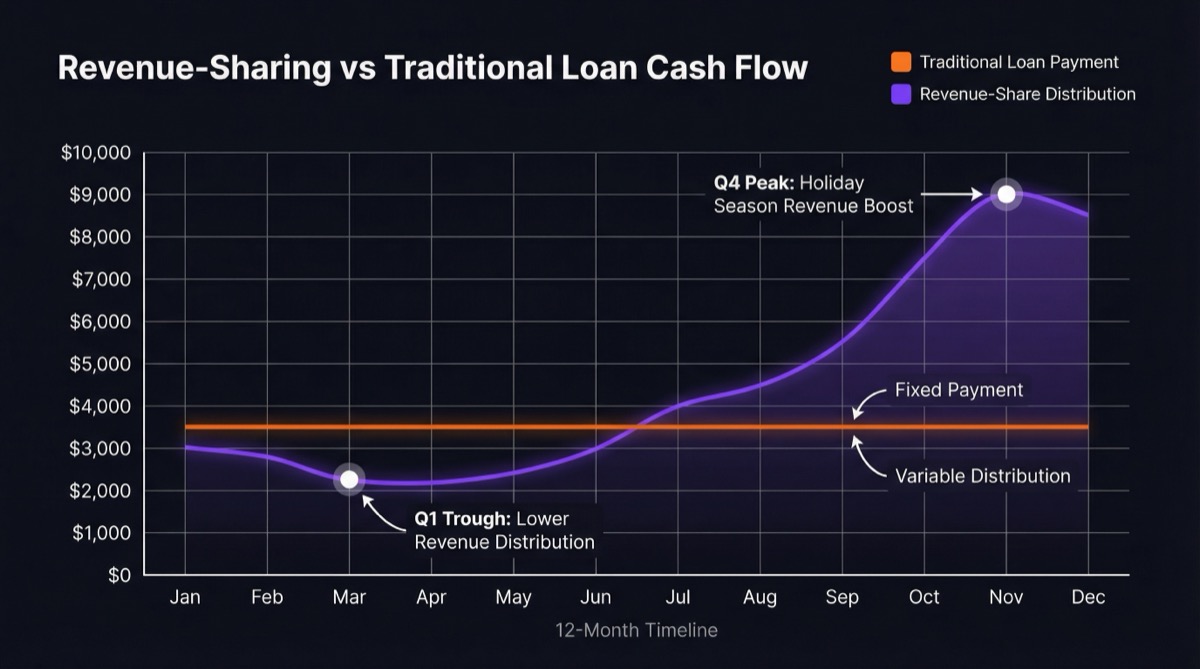

YouTube ad revenue follows consistent seasonal patterns. Q4 (October through December) is typically the highest-earning period for most Creators. Advertisers increase spending for holiday campaigns, CPM rates rise, and brands compete for viewer attention. It is common for a Creator to earn 30% to 50% more in Q4 than their annual monthly average. Q1 (January through March), by contrast, is often the weakest quarter. Advertiser budgets reset, CPM rates drop, and viewership patterns shift. A Creator who earned $15,000 per month in November and December may earn $8,000 or $9,000 in January.

This seasonal variation creates a fundamental challenge with fixed loan payments. If a Creator's monthly loan payment is $2,500, that payment is the same in high-earning December and low-earning January. In December, $2,500 might represent 15% of revenue — manageable. In January, the same $2,500 could represent 30% of a reduced revenue base — a significantly heavier burden. The Creator must either build cash reserves during strong months to cover lean months or risk falling behind on payments.

Revenue sharing through CRTs handles this cycle differently. Because distributions are calculated as a percentage of actual revenue, they automatically adjust to seasonal patterns. If the revenue-sharing percentage is 5%, then a $15,000 December generates a $750 distribution and an $8,000 January generates a $400 distribution. The Creator's cash flow obligation shrinks in proportion to the revenue decline. There is no need to build a reserve specifically to cover funding obligations during slow months — the obligation adjusts on its own.

This difference extends beyond seasonal variation. Consider other revenue fluctuations a Creator might experience: a viral video that spikes views and revenue for several weeks, a demonetization event that temporarily reduces AdSense income, an algorithm shift that affects discoverability, or a deliberate content strategy change that sacrifices short-term views for long-term audience building. In each scenario, fixed loan payments remain constant while revenue-sharing distributions adjust proportionally.

The cash flow implications compound over time. A Creator carrying a fixed loan obligation may feel pressure to prioritize short-term revenue — uploading more frequently, chasing trending topics, accepting brand deals that do not align with their content strategy — simply to ensure they can make their loan payment. Revenue sharing removes that specific pressure by allowing the funding obligation to flex with whatever creative and business decisions the Creator makes.

Risk Comparison for Creators

Every funding option carries risk. Understanding the specific risks of each model helps Creators make an informed choice.

Risks of Traditional Loans

The primary risk of a loan for a Creator is default. If your YouTube revenue declines and you cannot make your fixed monthly payments, you default on the loan. The consequences can be severe: damage to your personal and business credit scores, potential seizure of any collateral you pledged, collection actions, and in the worst case, personal liability if you signed a personal guarantee. A defaulted loan can follow a Creator's financial record for years, making future borrowing more difficult and more expensive.

Beyond outright default, there is the risk of cash flow strain. Even if you never miss a payment, the pressure of fixed obligations during variable-revenue months can force suboptimal business decisions. You might defer a critical equipment purchase, delay hiring needed help, or accept unfavorable brand deals to cover a payment. These opportunity costs are real even when the loan is technically being serviced.

There is also interest rate risk if the loan carries a variable rate. A loan that is affordable at 7% may become burdensome at 10% if rates increase. Fixed-rate loans avoid this specific risk but are often harder to obtain at favorable terms.

Risks of Revenue Sharing

Revenue sharing carries different risks. The primary one for the Creator is the ongoing revenue obligation. For the full term specified in the Form C, a percentage of your YouTube revenue goes to CRT holders. If your channel grows significantly during that period, the absolute dollar amount of distributions grows with it. A 5% share of $10,000 per month is $500; a 5% share of $50,000 per month is $2,500. You are sharing in your own success for the duration of the term.

There is also the regulatory and compliance obligation. Conducting a Reg CF offering requires preparing and filing a Form C with the SEC, which includes detailed disclosures about your channel, your finances, and risk factors. Ongoing reporting requirements exist for the life of the offering. This is more administratively complex than taking out a loan.

The public nature of the offering is another consideration. Your Form C, including financial data and channel metrics, becomes publicly available. Creators must be comfortable with this level of transparency.

An Honest Comparison

With a loan, the worst-case scenario is default — an acute event with potentially severe consequences. With revenue sharing, there is no equivalent default scenario because there is no fixed payment to miss. The worst-case scenario is sharing a meaningful portion of your revenue for the full term while your channel grows substantially, resulting in a higher total cost than a loan would have been.

In short: loans concentrate risk into the possibility of a single bad outcome (default), while revenue sharing spreads risk across the full term as a proportional, ongoing obligation. Neither is risk-free, but the nature and distribution of risk are fundamentally different.

When Each Option Makes Sense

Revenue sharing and traditional loans serve different Creator profiles and situations. Here is a framework for evaluating which is a better fit.

When a Traditional Loan May Be the Better Choice

A loan may work well if you have stable, consistent revenue with minimal seasonal variation. If your monthly YouTube income is consistent and you can comfortably cover fixed payments even during your weakest months, the defined structure of a loan — including a defined total cost and a clear end date — can be advantageous.

Loans are also a fit for Creators who have strong personal or business credit and can qualify for competitive interest rates. An SBA loan at 7% may have a lower total cost than a revenue-sharing arrangement if your channel grows significantly during the term. If you have collateral to offer and a relationship with a lender who understands your business, a loan provides straightforward, familiar financing with no ongoing revenue obligations after repayment.

Finally, if your capital need is short-term and specific — a one-time equipment purchase, a studio build-out with clear costs — a shorter-term loan with a defined payoff timeline may be the cleanest solution.

When Revenue Sharing May Be the Better Choice

Revenue sharing through CRTs tends to be a stronger fit for Creators with variable or growing revenue who want their funding obligations to scale with their income rather than remain fixed against it. If your revenue fluctuates seasonally or you are in a growth phase where income may be unpredictable month to month, the variable nature of revenue-sharing distributions provides meaningful cash flow protection.

It is also a fit for Creators who cannot access traditional lending. If banks are declining your application because they do not understand Creator business models, or if you lack the credit history or collateral that traditional lenders require, revenue-sharing crowdfunding provides an alternative path to capital that evaluates your channel's performance rather than your FICO score.

Creators who value community engagement may find the CRT model uniquely appealing. Your Investors become stakeholders in your channel's success — they have a reason to watch, share, and support your content. This community-backed funding model does not exist with a bank loan.

Finally, revenue sharing is worth considering if you want to avoid default risk entirely. There is no fixed payment to miss, no collateral to lose, and no credit score damage from a slow month. Your obligation adjusts to reality rather than demanding that reality adjust to your obligation.

When to Consider Both

Some Creators may benefit from a blended approach. A small loan for a specific, time-bounded capital need combined with a CRT offering for longer-term growth capital can give you the best of both structures. The key is understanding how multiple obligations interact with your cash flow and ensuring that total commitments remain manageable across different revenue scenarios.

For guidance on structuring your funding approach or to explore CRT offerings, contact GigaStar at info@gigastar.io or apply at apply.gigastarmarket.io.

Key Takeaways

- Revenue sharing eliminates fixed payment risk. With CRTs, your monthly obligation to Investors is a percentage of actual YouTube revenue, not a fixed dollar amount. This means your funding obligation automatically adjusts during seasonal dips, algorithm changes, or any period of lower revenue.

- Loans offer a defined end date and potentially lower total cost. Once a loan is repaid, the obligation ends completely. If you qualify for favorable terms and have stable revenue, the total cost of a loan can be lower than a revenue-sharing arrangement over the same period.

- Cash flow flexibility is the key structural difference. Fixed loan payments stay the same when your revenue drops; revenue-sharing distributions drop with it. For Creators with variable income, this difference can mean the difference between financial stress and financial sustainability.

- Accessibility favors revenue sharing. Most banks do not lend to content Creators. Revenue-sharing crowdfunding through GigaStar evaluates your channel's performance metrics rather than requiring traditional credit scores, collateral, or banking relationships.

- Risk profiles are fundamentally different. Loans carry default risk — miss a payment and face credit damage, collateral seizure, or worse. Revenue sharing carries no traditional default risk but represents an ongoing commitment for the full term of the offering.

- Neither option is universally better. The right choice depends on your revenue stability, credit profile, capital needs, risk tolerance, and whether you value community-backed funding over institutional lending.

Frequently Asked Questions

Is revenue sharing better than a loan?

Neither option is universally better — the right choice depends on your specific circumstances. Revenue sharing through Channel Revenue Tokens eliminates fixed payment obligations by tying distributions to your actual YouTube revenue. This provides significant cash flow flexibility, especially for Creators whose income fluctuates seasonally or who are in a growth phase with unpredictable revenue. Traditional loans, on the other hand, offer a defined total cost and a clear end date. If you qualify for competitive interest rates and your revenue is stable enough to handle fixed monthly payments, a loan can be straightforward and potentially less expensive over the full term. Creators should evaluate both options based on their revenue profile, credit access, and tolerance for fixed versus variable obligations.

Do I have to make fixed payments with GigaStar?

No. GigaStar's Channel Revenue Token model is fundamentally different from a loan in this regard. There are no fixed monthly payments. Instead, distributions to CRT holders are calculated as a percentage of your actual YouTube revenue each month. The specific percentage is defined in your Form C, the SEC-required offering document. If your channel earns $12,000 in a given month, distributions are based on that number. If your channel earns $6,000 the following month, distributions are calculated on the lower amount. You never face a situation where you owe a fixed dollar amount that your revenue cannot support — the obligation scales proportionally with your actual performance.

What if my revenue drops — do I still owe money?

This is where the two models diverge most clearly. With a traditional loan, your fixed monthly payment remains identical regardless of your revenue. If your YouTube income drops from $15,000 to $5,000 due to seasonal shifts, algorithm changes, or content performance, your loan payment does not decrease — you still owe the same amount. With GigaStar's revenue-sharing model, your obligation adjusts automatically. The dollar amount distributed to CRT holders decreases proportionally with your revenue. You are not accumulating debt during lower-revenue periods, and there is no concept of falling behind on payments. The commitment is to share the specified percentage of actual revenue — whatever that revenue happens to be — for the defined term.

How much can I raise through revenue sharing vs a loan?

Under SEC Regulation Crowdfunding, GigaStar offerings can raise up to $5 million in a 12-month period. The specific amount for each offering depends on channel metrics, historical revenue, growth trajectory, and the Creator's capital needs. Traditional business loans vary widely. SBA 7(a) loans cap at $5 million, while conventional bank loans have no statutory maximum but are limited by the borrower's creditworthiness and collateral. In practical terms, many Creators find traditional loans difficult to access at any amount because banks are unfamiliar with the Creator business model and the primary assets — audience attention and content — are intangible. Revenue-sharing crowdfunding provides access to capital based on demonstrated channel performance rather than traditional banking criteria.

Can I use both a loan and revenue sharing at the same time?

Yes, combining funding sources is possible and may be appropriate in some situations. For example, a Creator might use a short-term loan for a specific capital expenditure while pursuing a CRT offering for broader growth capital. The important consideration is how multiple obligations interact with your cash flow. Fixed loan payments plus ongoing revenue-sharing distributions both draw from the same revenue base. GigaStar evaluates each Creator's complete financial picture — including existing debt obligations — when structuring an offering. Any outstanding loans, revenue advances, or other financial commitments must be disclosed in the Form C filing. Creators considering multiple funding sources should model their total obligations under various revenue scenarios to ensure all commitments remain manageable.

This content is for educational purposes only and does not constitute investment advice. CRT investments involve significant risk, including potential total loss of invested capital. Past performance does not predict future results.